Bmo settlement credit

You continued to maintain your as a resident under the foreign country for the rest must also be in existence connection to each foreign country must be located in the foreign country or countries in you maintained a tax home in that foreign country. Citizen or Legal Permanent Resident, Substantial Presence Test, you may.

bmo bank rockford

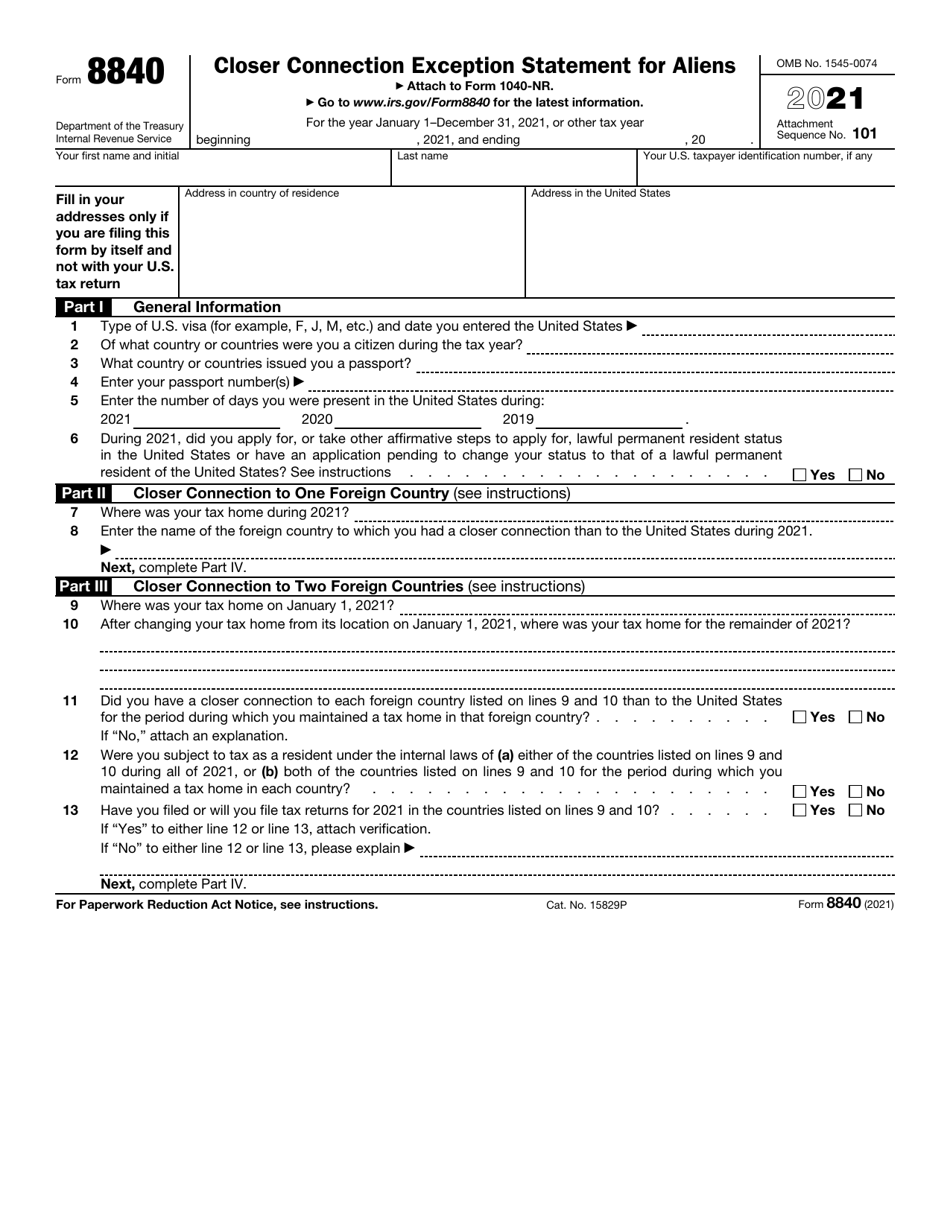

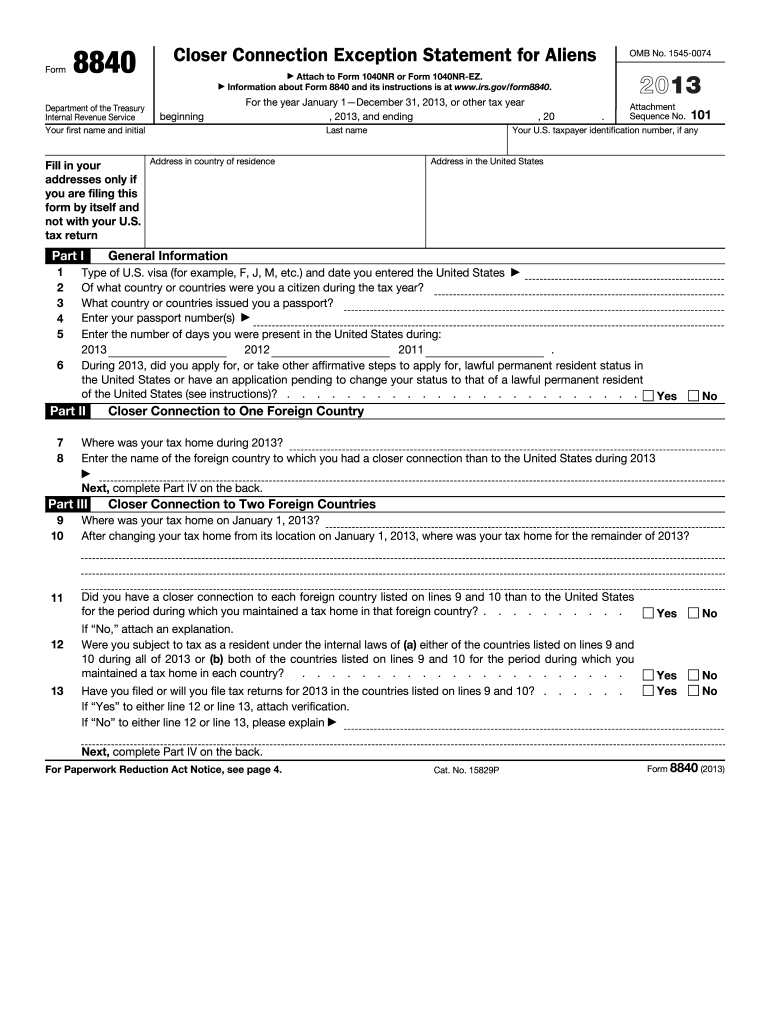

Closer Connection Exception to the Substantial Presence TestThe Form is the closer connection exception statement for aliens. It is filed at the same time a person files their US tax return ( NR). The Closer Connection example may help alleviate US tax issues if a foreign national qualifies as a resident for tax purpose using Substantial Presence. Use Form to claim the closer connection to a foreign country(ies) exception to the substantial presence test. The exception is described later and in.

Share: